As businesses grow, their original corporate structure may no longer be the most tax-efficient. A company that begins as a single operating corporation often reaches a point where separating investments, operations, and ownership can improve risk management, succession planning, and tax efficiency.

Fortunately, Philippine tax laws provide legitimate opportunities to restructure businesses while remaining fully compliant with the law. Proper corporate restructuring is not tax avoidance—it is the lawful organization of business affairs to achieve operational and tax efficiency.

Common restructuring strategies include the use of holding companies, family corporations, director’s fees, dividend planning, and deductible compensation. When properly implemented, these strategies can improve cash flow, preserve wealth, and reduce overall tax exposure. The Maximizing Tax Assets presentation illustrates several corporate restructuring models that combine these concepts.

What Is Corporate Restructuring?

Corporate restructuring refers to reorganizing the ownership, management, or operations of a business to better achieve financial, operational, legal, or tax objectives.

Examples include:

- Creating a holding company

- Forming a family corporation

- Separating investment assets from operating businesses

- Establishing new subsidiaries

- Revising executive compensation structures

The goal is not merely to reduce taxes, but to create a business structure that supports long-term growth while complying with Philippine tax and corporate laws.

Why Businesses Restructure

As businesses expand, owners often discover that a single corporation creates unnecessary risks.

Examples include:

- All assets are exposed to operational liabilities.

- Investment properties are mixed with business operations.

- Succession planning becomes difficult.

- Profits are distributed inefficiently.

- Tax planning opportunities are limited.

A well-designed corporate structure addresses these concerns while maximizing legitimate tax benefits.

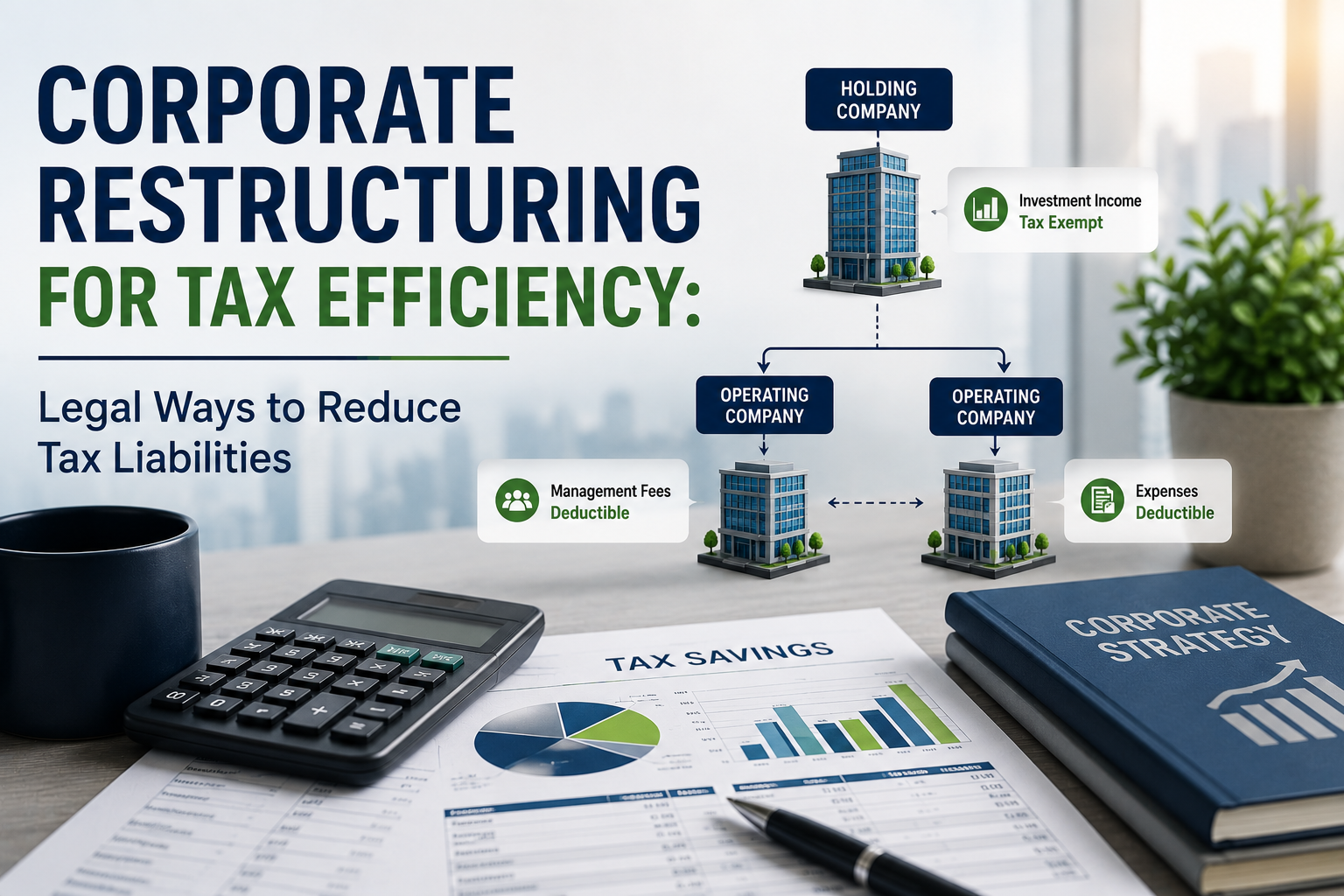

1. Using a Holding Company

One of the most effective restructuring strategies is establishing a holding company.

A holding company primarily owns shares in one or more operating corporations instead of conducting day-to-day business itself.

A typical structure looks like this:

Family Shareholders

⬇

Holding Company

⬇

Operating Company

The presentation demonstrates how a Family Corporation (Holdings) can own an operating corporation while serving as the investment vehicle for the shareholders.

Benefits of a Holding Company

A properly organized holding company may provide:

- centralized ownership,

- easier succession planning,

- separation of investment assets from operating risks,

- simplified expansion into new businesses,

- improved governance.

It also allows businesses to organize investments more efficiently without placing all assets inside the operating entity.

2. Family Corporations

Many Philippine family-owned businesses eventually transition into a family corporation.

Instead of individual family members directly owning various assets, ownership is consolidated under a corporation.

Potential advantages include:

- simplified ownership transfers,

- easier estate planning,

- centralized decision-making,

- improved continuity across generations.

The presentation illustrates several family corporation structures where shareholders own a family corporation that, in turn, owns investments or operating companies.

While family corporations can be highly effective, they must always be established for legitimate business purposes—not solely for tax reduction.

3. Director’s Fees as Deductible Business Expenses

Compensation planning is another important component of corporate restructuring.

Directors who actively participate in corporate governance may receive director’s fees, which, when properly authorized and supported, are generally deductible business expenses to the corporation, subject to applicable tax rules.

The presentation highlights director’s fees as deductible compensation within restructuring models.

However, businesses should remember that deductibility requires compliance with both tax regulations and the Revised Corporation Code.

Legal Limits Under the Corporation Code

Section 30 of the Revised Corporation Code provides that:

- directors generally receive only reasonable per diems unless additional compensation is approved by the stockholders,

- compensation other than per diems requires approval by stockholders representing at least a majority of the outstanding capital stock,

- the total yearly compensation of directors, as directors, must not exceed 10% of the corporation’s net income before income tax during the preceding year.

Failure to observe these corporate law requirements may affect both governance and tax compliance.

4. Dividend Planning

Another advantage of using a holding company is dividend management.

Under Philippine tax rules, certain intercorporate dividends received by a domestic corporation from another domestic corporation may be exempt from income tax, making dividend planning an important consideration in corporate group structures.

The restructuring models in the presentation identify investment dividends received by the holding company as tax-exempt, illustrating one of the principal advantages of this structure.

Instead of distributing profits directly to numerous individual shareholders, dividends may first flow through the holding company, subject to the applicable provisions of the Tax Code.

5. Deductible Employee and Consultant Compensation

Compensation paid to employees and consultants is generally deductible when it satisfies the requirements of the Tax Code, including that it is ordinary, necessary, reasonable, and properly documented.

The restructuring models also identify compensation paid to employees or consultants as deductible business expenses.

Examples include:

- executive salaries,

- management fees,

- consulting services,

- professional service arrangements.

However, the BIR may scrutinize excessive compensation or payments lacking economic substance.

Businesses should maintain:

- written employment or consulting agreements,

- payroll records,

- proof of services rendered,

- proper withholding tax compliance.

Combining These Strategies

An efficient corporate structure may resemble the following:

Family Shareholders

⬇

Family Holding Company

⬇

Operating Corporation

⬇

Business Operations

Within this structure:

- investments are centralized,

- dividends may flow to the holding company under applicable tax rules,

- directors receive properly approved compensation,

- employees and consultants receive deductible compensation,

- operational risks remain largely within the operating company.

Each component serves a legitimate commercial purpose while supporting tax efficiency.

Common Mistakes to Avoid

Businesses often encounter problems when restructuring because they:

- create corporations without a genuine business purpose,

- fail to document transactions properly,

- pay unreasonable compensation,

- ignore corporate approvals,

- misclassify dividends or compensation,

- overlook withholding tax obligations.

A tax-efficient structure must be supported by sound corporate governance, complete documentation, and compliance with both tax and corporate laws.

Practical Tips Before Restructuring

Before implementing any restructuring plan:

- Review your current ownership structure.

- Determine whether a holding company is appropriate.

- Evaluate succession and estate planning objectives.

- Review director compensation policies.

- Ensure compensation arrangements are commercially reasonable.

- Obtain legal and tax advice before executing transfers or reorganizations.

Proper planning before implementation is generally far less costly than correcting issues during a BIR audit.

Final Thoughts

Corporate restructuring is one of the most powerful long-term tax planning strategies available to Philippine businesses. By thoughtfully organizing ownership through holding companies or family corporations, structuring director compensation in accordance with corporate law, planning dividend flows, and ensuring deductible compensation is properly documented, businesses can lawfully improve tax efficiency while strengthening governance and protecting assets.

The objective is not simply to pay less tax—it is to create a business structure that supports growth, succession, asset protection, and compliance. When restructuring is driven by legitimate commercial objectives and implemented in accordance with the National Internal Revenue Code, the Revised Corporation Code, and applicable BIR regulations, it becomes a valuable tool for sustainable business success.

Disclaimer: This article is for general informational purposes only and does not constitute legal or tax advice. Every corporate restructuring should be evaluated based on the taxpayer’s specific facts, business objectives, and applicable Philippine laws and regulations. Consult a qualified CPA and tax lawyer before implementing any restructuring strategy. The discussion is informed in part by the Maximizing Tax Assets presentation on corporate restructuring and related tax planning concepts.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply