One of the most expensive tax mistakes in real estate transactions is the improper classification of property as either an ordinary asset or a capital asset. A simple error in classification can increase tax liabilities by millions of pesos—or expose a taxpayer to costly Bureau of Internal Revenue (BIR) assessments, surcharges, and penalties.

Many taxpayers assume that all real property sales are taxed the same way. In reality, the tax consequences depend primarily on how the property is classified under the National Internal Revenue Code (NIRC). The applicable taxes may include Income Tax, Value-Added Tax (VAT), Capital Gains Tax (CGT), and Documentary Stamp Tax (DST), and the amount due can vary significantly. The Maximizing Tax Assets presentation emphasizes the importance of distinguishing between ordinary and capital assets before determining the applicable taxes.

This article explains the differences between ordinary and capital assets, compares their tax treatment, and discusses why proper classification is an essential part of tax planning.

Understanding Asset Classification

Before computing taxes, the first question every taxpayer should ask is:

“Is the property an ordinary asset or a capital asset?”

The answer determines which taxes apply.

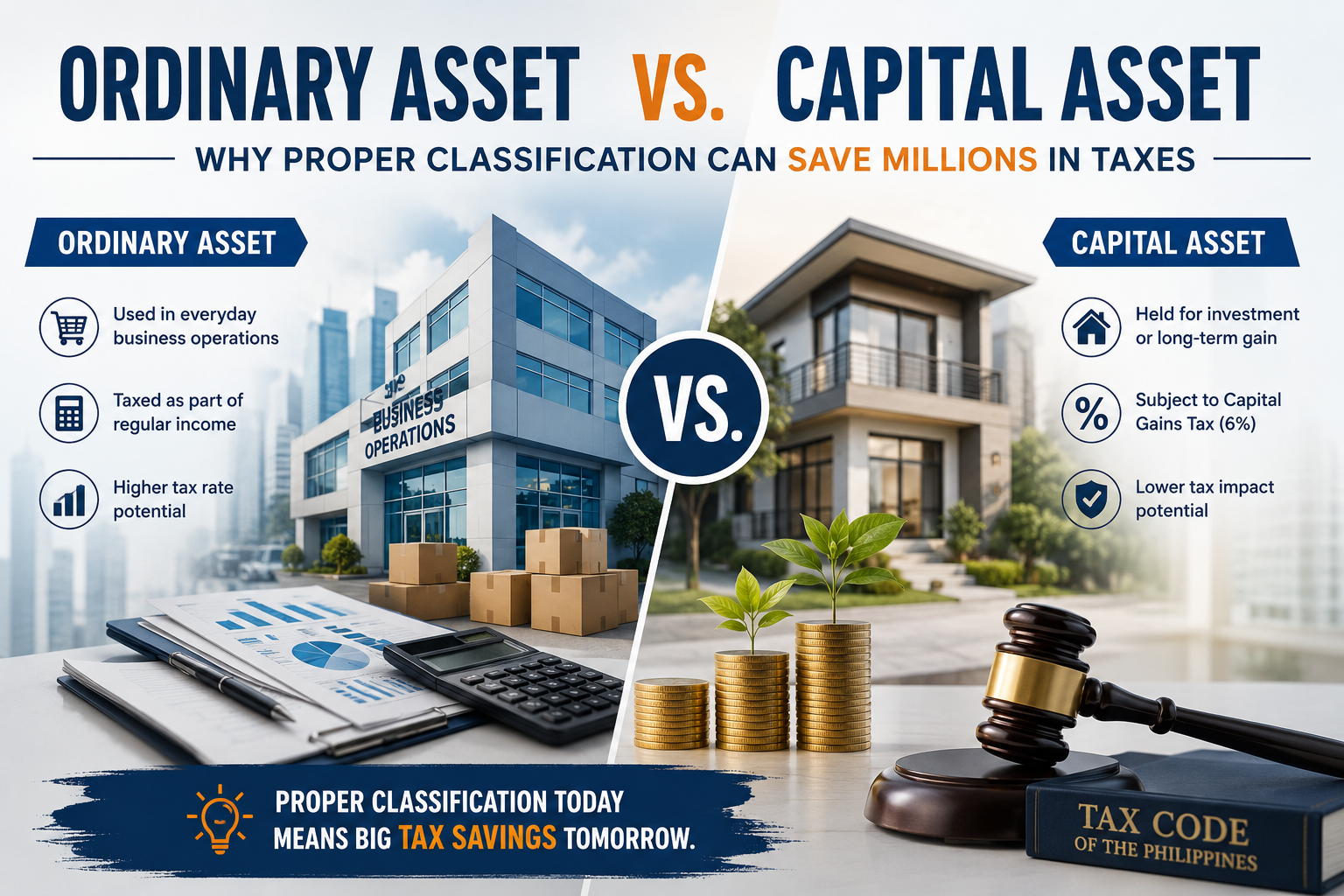

What Is an Ordinary Asset?

Under the Tax Code, ordinary assets include real properties that are used or held in connection with a trade or business.

These generally include:

- Real property held primarily for sale to customers in the ordinary course of business;

- Property included in inventory;

- Buildings and improvements subject to depreciation; and

- Real property used in the taxpayer’s trade or business.

Examples

A property is generally considered an ordinary asset if it is:

- Inventory of a real estate developer

- A warehouse used by a manufacturing company

- An office building used in business operations

- Commercial property leased as part of business activities

What Is a Capital Asset?

A capital asset is generally any real property that is not classified as an ordinary asset.

Typically, these include properties held for investment or personal purposes rather than for business operations.

Examples include:

- Residential lots held for investment

- Vacation homes

- Personal residential properties

- Idle land not used in business

The Tax Code defines capital assets as properties not falling within the statutory definition of ordinary assets.

Why Classification Matters

The classification directly affects the taxes imposed upon sale.

The same parcel of land sold for the same amount may produce vastly different tax liabilities depending on whether it is treated as an ordinary asset or a capital asset.

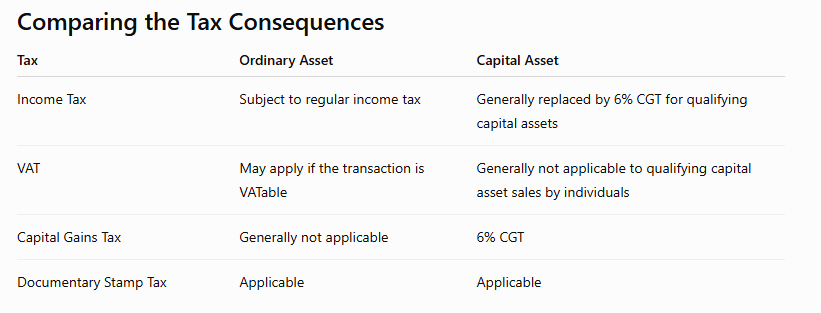

Tax Consequences of Selling an Ordinary Asset

When an ordinary asset is sold, the transaction is generally subject to:

1. Income Tax

Instead of the 6% Capital Gains Tax applicable to qualifying capital assets, the gain from selling an ordinary asset is generally subject to the applicable income tax regime.

For corporations, the gain is generally taxed under the regular corporate income tax rules.

For individuals engaged in business, the gain becomes part of taxable income subject to the graduated income tax rates.

2. Value-Added Tax (VAT)

If the seller is VAT-registered and the sale is VATable under the Tax Code, the sale of an ordinary asset may also be subject to 12% VAT.

This often represents one of the largest additional tax costs.

3. Documentary Stamp Tax (DST)

Transfers of real property are likewise generally subject to Documentary Stamp Tax in accordance with applicable tax rules.

Tax Consequences of Selling a Capital Asset

The tax treatment changes significantly when the property qualifies as a capital asset.

1. Capital Gains Tax (CGT)

The sale is generally subject to a 6% Capital Gains Tax, computed on the higher of:

- Gross Selling Price, or

- Fair Market Value (including the applicable zonal value, where relevant).

The tax is imposed regardless of the seller’s actual gain or loss.

2. No VAT (Generally)

Unlike ordinary assets, the sale of a capital asset by an individual is generally not subject to VAT.

This distinction alone may produce substantial tax savings.

3. Documentary Stamp Tax (DST)

DST generally remains applicable to the transfer of real property.

The presentation provides an illustrative computation showing that a sale of an ordinary asset may result in combined Income Tax, VAT, and DST significantly exceeding the taxes due on a comparable sale of a capital asset, where only CGT and DST generally apply.

A Practical Illustration

Assume a property is sold for ₱50 million.

If classified as an ordinary asset, the seller may become liable for:

- Regular Income Tax;

- 12% VAT (if applicable);

- Documentary Stamp Tax.

If the same property qualifies as a capital asset, the transaction may instead be subject primarily to:

- 6% Capital Gains Tax; and

- Documentary Stamp Tax.

The Maximizing Tax Assets presentation illustrates a scenario in which the total taxes on an ordinary asset sale substantially exceed those on a comparable capital asset sale, demonstrating how proper classification can result in significant tax savings.

Common Classification Errors

Many taxpayers unknowingly misclassify their properties.

Common mistakes include:

- Assuming that all land owned by a corporation is automatically an ordinary asset.

- Treating investment property used in business as a capital asset.

- Ignoring changes in property use over time.

- Failing to consider whether a depreciable building has become an ordinary asset.

- Relying solely on the property’s title rather than its actual use.

The BIR examines both the legal and factual circumstances surrounding the property when determining its classification.

Tax Planning Considerations

Proper tax planning begins before the sale.

Businesses and investors should evaluate:

- The property’s actual use.

- Whether it forms part of business inventory.

- Whether it is depreciable.

- Whether it is held primarily for investment.

- The seller’s taxpayer classification.

- Applicable VAT rules.

- Available exemptions or special tax provisions.

Early planning helps prevent costly surprises at the closing stage.

When Professional Advice Matters

Real estate transactions frequently involve multiple taxes and significant amounts.

Before selling valuable property, taxpayers should consult experienced CPAs and tax lawyers to:

- determine the correct asset classification;

- compute all applicable taxes accurately;

- evaluate available exemptions;

- ensure compliance with BIR documentary requirements; and

- avoid assessments, penalties, and interest.

Proper documentation is often just as important as proper classification.

Final Thoughts

The distinction between an ordinary asset and a capital asset is more than a technical tax concept—it is one of the most important determinants of the taxes payable on a real property sale in the Philippines.

A property classified as an ordinary asset may be subject to regular income tax, VAT, and DST, while a qualifying capital asset sale may instead be subject primarily to Capital Gains Tax and DST. These differences can translate into substantial tax savings—or unexpected tax costs—depending on the facts of each transaction.

For business owners, investors, and property holders, understanding this distinction is essential. Proper asset classification, supported by accurate documentation and professional tax advice, can help ensure compliance with Philippine tax laws while preserving significant value.

Disclaimer: This article is intended for general informational purposes only and should not be construed as legal or tax advice. The proper classification of real property depends on the taxpayer’s specific facts, the property’s actual use, and the applicable provisions of the National Internal Revenue Code, BIR regulations, and relevant jurisprudence. Consult a qualified CPA and tax lawyer before entering into any real estate transaction. The discussion is informed in part by the Maximizing Tax Assets presentation.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply