If you’re a freelancer, professional, online seller, consultant, or sole proprietor in the Philippines, one of the most important tax decisions you’ll make each year is choosing the correct Annual Income Tax Return (AITR). Many self-employed taxpayers become confused between BIR Form 1701 and BIR Form 1701A, often resulting in filing errors, delayed compliance, or even penalties.

Although both forms are designed for self-employed individuals, they are not interchangeable. Each form has its own eligibility requirements, tax options, and filing rules under the National Internal Revenue Code (NIRC), the Tax Reform for Acceleration and Inclusion (TRAIN) Law, and Bureau of Internal Revenue (BIR) regulations.

This guide explains the differences between BIR Form 1701 and BIR Form 1701A, who should file each form, and how to determine which return best applies to your situation.

Understanding Annual Income Tax Returns

Every individual engaged in business or the practice of a profession is generally required to file an Annual Income Tax Return (AITR) unless exempt under applicable laws.

The annual return reports:

- Gross income

- Allowable deductions

- Taxable income

- Tax credits

- Income tax due

- Taxes already paid during the year

Choosing the correct form ensures that your tax computation is consistent with your registered tax classification and elected tax regime.

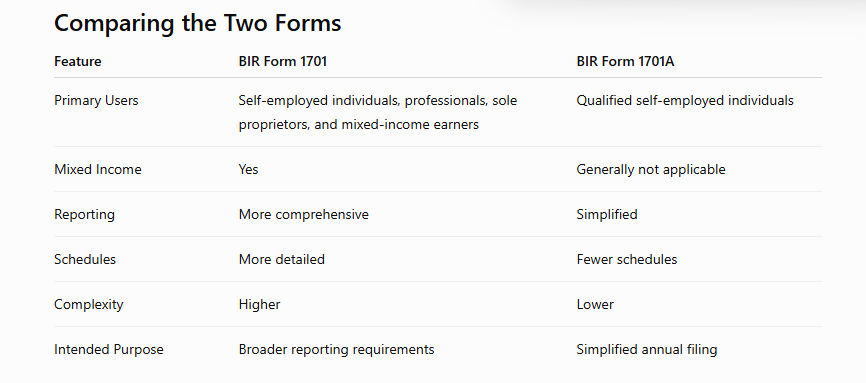

What Is BIR Form 1701?

BIR Form 1701 is the Annual Income Tax Return generally used by:

- Sole proprietors

- Self-employed individuals

- Licensed professionals

- Freelancers

- Consultants

- Mixed-income earners (individuals earning both compensation income and business or professional income)

The form accommodates taxpayers whose income tax computation may involve different tax regimes or more comprehensive reporting requirements.

Because it is designed for a broader range of taxpayers, Form 1701 contains additional schedules and disclosures compared with Form 1701A.

What Is BIR Form 1701A?

BIR Form 1701A is a simplified Annual Income Tax Return intended for qualified self-employed individuals.

It was introduced following the implementation of the TRAIN Law to simplify tax compliance for taxpayers who qualify under specific income tax options.

Compared with Form 1701, Form 1701A:

- contains fewer schedules;

- requires less detailed reporting;

- is easier to accomplish;

- simplifies income tax computation.

However, not every self-employed taxpayer qualifies to use it.

Who Should File BIR Form 1701?

Generally, BIR Form 1701 applies to:

Sole Proprietors

Individuals operating registered businesses under their own names.

Examples:

- Retail store owners

- Restaurant operators

- Contractors

- Traders

Professionals

Individuals practicing a profession independently.

Examples:

- Lawyers

- Certified Public Accountants

- Doctors

- Architects

- Engineers

- Dentists

Freelancers

Examples include:

- Graphic designers

- Software developers

- Virtual assistants

- Digital marketers

- Writers

- Content creators

Mixed-Income Earners

Individuals who receive:

- compensation income from employment; and

- business or professional income.

Because both income sources must generally be reported together, Form 1701 is usually the appropriate return.

Who May Use BIR Form 1701A?

Form 1701A is generally intended for qualified self-employed individuals who satisfy the requirements prescribed by the BIR.

Typical examples include:

- Sole proprietors

- Freelancers

- Professionals

- Online sellers

provided they qualify under the applicable tax regime and are not required to use Form 1701 because of their income classification or other circumstances.

Eligibility should always be confirmed based on the taxpayer’s BIR registration and elected tax treatment.

Tax Options Under Form 1701

One reason Form 1701 is more comprehensive is that it accommodates taxpayers who may be subject to different methods of income tax computation.

Depending on the taxpayer’s circumstances and applicable laws, income tax may be computed using:

- Graduated income tax rates;

- Optional deduction methods available under the Tax Code; or

- Other applicable tax treatments.

Because of these possibilities, Form 1701 requires more detailed reporting.

Tax Options Under Form 1701A

Form 1701A is intended to simplify reporting for qualified taxpayers using the tax options available to them under current law.

Depending on the taxpayer’s registration and election with the BIR, this may include:

- Graduated income tax rates with allowable deductions; or

- The 8% income tax option, if the taxpayer qualifies and has validly elected it under applicable regulations.

The form is designed to streamline reporting while remaining compliant with Philippine tax laws.

Filing Requirements

Regardless of which return applies, taxpayers should prepare:

- Books of account

- Financial records

- Sales records

- Expense records

- BIR Forms 2307 (if applicable)

- Proof of taxes previously paid

- Supporting schedules

- Other documents required by the BIR

Accurate documentation remains essential regardless of which form is used.

Common Filing Mistakes

Many self-employed taxpayers encounter compliance issues because of avoidable mistakes.

1. Using Form 1701A Without Qualifying

Some taxpayers choose Form 1701A simply because it appears easier.

However, eligibility—not convenience—determines which form should be filed.

2. Forgetting Mixed Income

Employees with side businesses often mistakenly file only Form 1700 or incorrectly use Form 1701A.

Mixed-income earners generally have different reporting obligations.

3. Incorrect Tax Regime

The income tax return must be consistent with the taxpayer’s registered tax treatment and elections made with the BIR.

Changing tax computation methods without proper compliance may create filing issues.

4. Incomplete Tax Credit Claims

Taxpayers frequently overlook:

- BIR Form 2307 credits;

- quarterly income tax payments;

- excess tax credits.

Failure to claim legitimate tax credits may result in unnecessary tax payments.

5. Poor Recordkeeping

Incomplete accounting records often lead to:

- incorrect income reporting;

- unsupported deductions;

- inaccurate tax computations.

Maintaining organized financial records throughout the year makes annual filing significantly easier.

Practical Tips Before Filing

Before preparing your Annual Income Tax Return:

- Verify your taxpayer classification with the BIR.

- Confirm whether you are registered as purely self-employed or as a mixed-income earner.

- Review your elected income tax option.

- Reconcile quarterly tax returns with your accounting records.

- Gather all BIR Forms 2307 and other tax credit documents.

- Ensure that income and deductions are fully supported.

- Consult a CPA or tax lawyer if your tax situation is complex.

Proper planning before filing can prevent costly amendments and compliance issues.

Final Thoughts

Choosing between BIR Form 1701 and BIR Form 1701A is not simply a matter of selecting the shorter form—it depends on your taxpayer classification, sources of income, elected tax regime, and eligibility under Philippine tax laws.

For many self-employed taxpayers, Form 1701A offers a simplified filing process. However, taxpayers with mixed income or those who do not meet the eligibility requirements must generally use Form 1701.

Understanding these differences allows freelancers, professionals, entrepreneurs, and sole proprietors to comply with BIR requirements accurately while avoiding unnecessary penalties and maximizing legitimate tax benefits.

When uncertainty exists, seeking professional guidance before filing is always the wiser—and often less costly—decision.

Disclaimer: This article is intended for general informational purposes only and should not be construed as legal or tax advice. The appropriate income tax return depends on the taxpayer’s specific facts, BIR registration, income sources, elected tax regime, and applicable laws and regulations. Tax forms and filing requirements may change through legislation or BIR issuances. Consult a qualified CPA or tax lawyer to determine the correct return to file and to ensure compliance with Philippine tax laws.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply