For corporations operating in the Philippines, filing the correct Annual Income Tax Return (AITR) is more than a compliance requirement—it is a critical step in avoiding penalties, tax deficiencies, and unnecessary scrutiny from the Bureau of Internal Revenue (BIR).

One of the most common areas of confusion among corporate taxpayers is determining which version of BIR Form 1702 should be filed. Many corporations are aware that they must submit an annual income tax return, but are uncertain whether they should use BIR Form 1702-RT, BIR Form 1702-MX, or BIR Form 1702-EX.

Choosing the wrong form can result in filing errors, amended returns, and possible BIR assessments. Fortunately, the distinction is straightforward once you understand the corporation’s tax classification.

This guide explains the differences between the three corporate income tax returns, who should file each one, and how to determine the correct form for your business.

What Is BIR Form 1702?

BIR Form 1702 refers to the Annual Income Tax Return used by corporations and other non-individual taxpayers to report their taxable income for the year.

Unlike individual taxpayers who file BIR Forms 1700, 1701, or 1701A, corporations generally file one of the following:

- BIR Form 1702-RT

- BIR Form 1702-MX

- BIR Form 1702-EX

The applicable form depends primarily on the corporation’s tax treatment under the National Internal Revenue Code (NIRC).

Why Choosing the Correct Form Matters

Filing the proper annual income tax return ensures that the corporation:

- reports income accurately;

- applies the correct tax rules;

- claims allowable deductions and tax credits;

- complies with BIR regulations;

- avoids unnecessary amendments and penalties.

Using the wrong form may lead to delayed processing or additional compliance requirements during a BIR audit.

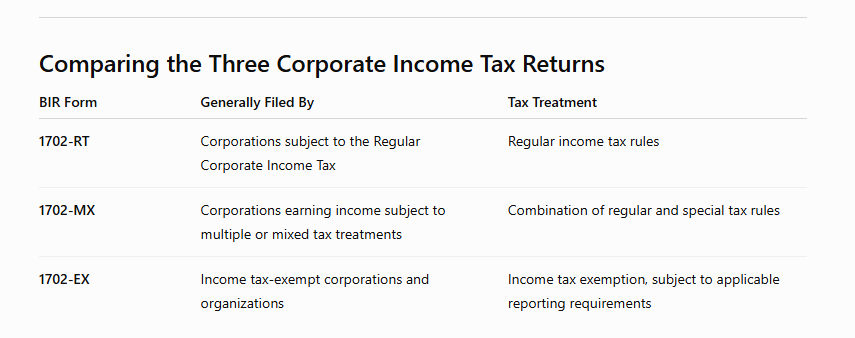

BIR Form 1702-RT

Annual Income Tax Return for Corporations Subject to the Regular Income Tax Rate

Who Should File?

BIR Form 1702-RT is generally filed by corporations that are subject to the Regular Corporate Income Tax (RCIT) under the Tax Code.

Examples include:

- Domestic corporations engaged in business

- Resident foreign corporations

- Corporations earning taxable business income

- Other corporations subject to the regular corporate income tax regime

These corporations compute income tax based on taxable income after allowable deductions.

What Is Reported?

Corporations filing Form 1702-RT generally report:

- Gross income

- Cost of sales or services

- Operating expenses

- Other income

- Allowable deductions

- Taxable income

- Income tax due

- Tax credits

- Creditable Withholding Taxes (CWT)

- Minimum Corporate Income Tax (MCIT), where applicable

- Net Operating Loss Carry-Over (NOLCO), if available

This is the most commonly used corporate income tax return.

BIR Form 1702-MX

Annual Income Tax Return for Corporations with Mixed Income Subject to Multiple Income Tax Rates or Special Tax Treatments

The “MX” in 1702-MX refers to mixed income or corporations whose income is subject to different tax treatments.

Who Should File?

Generally, Form 1702-MX applies to corporations that earn income subject to:

- regular corporate income tax; and

- special or preferential income tax treatments under the Tax Code or special laws.

Examples may include corporations with:

- income taxed at different rates;

- income enjoying preferential tax treatment;

- income subject to special tax regimes.

Because these corporations compute taxes using multiple tax treatments, Form 1702-MX contains additional schedules necessary to segregate the different categories of income.

BIR Form 1702-EX

Annual Income Tax Return for Corporations Exempt from Income Tax

Who Should File?

BIR Form 1702-EX is generally used by corporations and organizations that are exempt from income tax under the National Internal Revenue Code or special laws.

Examples may include:

- Non-stock, non-profit organizations that qualify for tax exemption

- Educational institutions enjoying income tax exemptions under applicable laws

- Certain government-owned or controlled corporations, where applicable

- Other entities specifically exempt from income tax

It is important to note that income tax exemption does not automatically exempt an organization from all tax obligations.

Many exempt organizations remain subject to:

- withholding tax requirements;

- documentary stamp tax;

- Value-Added Tax (VAT), where applicable;

- percentage tax, where applicable;

- other information return requirements.

How to Determine the Correct Form

Ask the following questions:

Is your corporation subject to the regular corporate income tax?

If yes, Form 1702-RT is generally the appropriate return.

Does your corporation earn income subject to more than one tax regime?

If the corporation has both regularly taxed income and income subject to preferential or special tax treatment, Form 1702-MX may be applicable.

Is your organization exempt from income tax?

If the corporation or organization qualifies for income tax exemption under the Tax Code or another applicable law, Form 1702-EX may generally be used.

Supporting Documents

Regardless of the form filed, corporations should prepare complete supporting documentation, including:

- Financial Statements

- Audited Financial Statements, when required

- Trial Balance

- General Ledger

- Income Tax Computations

- Tax Credit Schedules

- BIR Forms 2307

- Quarterly Income Tax Returns

- Other schedules required by the BIR

Accurate supporting documents strengthen compliance and reduce audit risks.

Common Filing Mistakes

Many corporations encounter avoidable compliance issues because of filing errors.

1. Using the Wrong Form

Some corporations automatically file Form 1702-RT without considering whether they qualify for another version of the return.

The applicable form depends on the corporation’s tax treatment—not simply its legal structure.

2. Failure to Reconcile Quarterly Returns

The annual return should reconcile with:

- quarterly income tax returns;

- financial statements;

- books of account;

- tax credit schedules.

Discrepancies often attract BIR attention.

3. Overlooking Tax Assets

Before filing, corporations should review:

- Creditable Withholding Taxes (CWT)

- Minimum Corporate Income Tax (MCIT)

- Net Operating Loss Carry-Over (NOLCO)

- Excess Input VAT

- Deferred Tax Assets

Failure to claim available tax assets may increase the corporation’s tax liability unnecessarily.

4. Incomplete Financial Statement Disclosures

Income tax disclosures should be consistent with:

- tax computations;

- deferred tax balances;

- tax credits;

- notes to the financial statements.

Proper disclosure strengthens both financial reporting and tax compliance.

5. Missing Filing Deadlines

Late filing may result in:

- surcharge;

- interest;

- compromise penalties;

- additional compliance issues.

Maintaining a corporate tax calendar helps ensure timely filing.

Best Practices Before Filing

Before preparing the Annual Income Tax Return, corporations should:

- Confirm their applicable tax classification.

- Determine the correct version of BIR Form 1702.

- Reconcile quarterly income tax returns.

- Review available tax credits and deductions.

- Verify financial statement balances.

- Update MCIT and NOLCO schedules.

- Gather all supporting tax documents.

- Consult a CPA or tax lawyer for complex transactions.

Proper planning minimizes filing errors and improves tax compliance.

Final Thoughts

Selecting the correct corporate income tax return is an essential part of tax compliance in the Philippines. Whether your corporation files BIR Form 1702-RT, 1702-MX, or 1702-EX depends not only on its legal structure but also on its tax classification and the nature of its income.

Understanding these distinctions helps corporations prepare accurate annual returns, claim legitimate tax benefits, and reduce the risk of costly BIR assessments. More importantly, proper filing supports sound corporate governance and strengthens the company’s overall tax compliance framework.

If there is uncertainty regarding the applicable form or tax treatment, seeking professional advice before filing is a prudent investment that can help prevent costly compliance issues in the future.

Disclaimer: This article is intended for general informational purposes only and should not be construed as legal or tax advice. The appropriate corporate income tax return depends on the corporation’s specific facts, tax classification, applicable provisions of the National Internal Revenue Code, BIR regulations and issuances, and relevant special laws. Filing requirements and tax forms may change over time. Corporations should consult a qualified CPA or tax lawyer to determine the correct BIR Form 1702 variant and ensure full compliance with Philippine tax laws.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply