Whether you’re a business owner, employer, freelancer, professional, or employee, you’ve likely encountered BIR Forms 2307, 2306, or 2316. While these certificates all relate to taxes withheld at source, they serve different purposes and apply to different types of income.

Confusing one certificate with another is a common mistake that can lead to incorrect tax reporting, denied tax credit claims, or compliance issues during a Bureau of Internal Revenue (BIR) audit.

This guide explains the differences between BIR Forms 2307, 2306, and 2316, who receives each certificate, when they are issued, and how they affect your tax obligations.

Why Withholding Tax Certificates Matter

The Philippine withholding tax system requires certain payors to withhold taxes before making payments to recipients.

The withheld taxes are then remitted to the Bureau of Internal Revenue (BIR).

To prove that taxes have been withheld and remitted, the withholding agent issues the appropriate BIR certificate.

These certificates serve several important purposes:

- Evidence of taxes withheld

- Support for tax credit claims

- Proof of tax compliance

- Documentation during BIR audits

- Verification of income received

Understanding which certificate applies helps ensure accurate tax reporting.

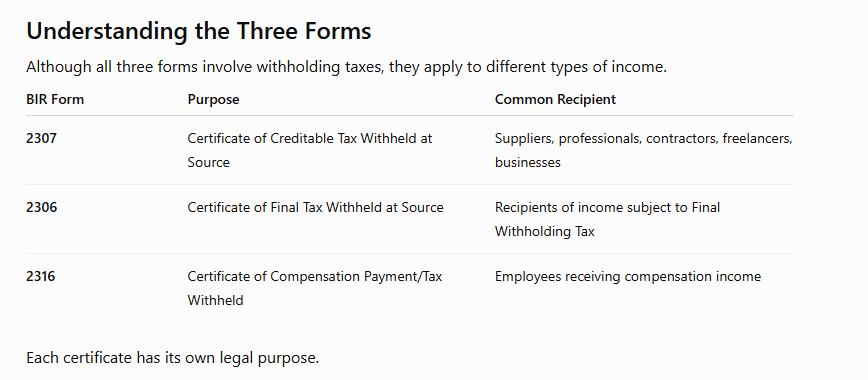

BIR Form 2307

Certificate of Creditable Tax Withheld at Source

BIR Form 2307 is issued when income is subject to Expanded Withholding Tax (EWT) or other Creditable Withholding Taxes (CWT).

The tax withheld is not the final tax.

Instead, it serves as an advance payment of the recipient’s income tax, which may later be credited against the recipient’s annual income tax liability.

Who Receives Form 2307?

Common recipients include:

- Independent professionals

- Consultants

- Lawyers

- Certified Public Accountants

- Architects

- Engineers

- Freelancers

- Contractors

- Suppliers

- Service providers

- Sole proprietors

- Corporations receiving income subject to Expanded Withholding Tax

Why Is It Important?

BIR Form 2307 allows the recipient to:

- claim tax credits;

- reduce quarterly income tax due;

- reduce annual income tax liability;

- support refund or carry-over claims where applicable.

Without Form 2307, taxpayers may find it difficult to substantiate creditable withholding tax claims.

BIR Form 2306

Certificate of Final Tax Withheld at Source

BIR Form 2306 is issued for income subject to Final Withholding Tax (FWT).

Unlike Form 2307, the tax withheld under Form 2306 generally fully satisfies the recipient’s income tax liability on that particular income.

The recipient ordinarily does not claim the tax withheld as a credit against another income tax obligation because the tax has already been finally paid through withholding.

Who Receives Form 2306?

Recipients may include taxpayers receiving income such as:

- Certain interest income

- Certain royalty income

- Certain dividend income

- Certain prizes and winnings

- Other income subject to Final Withholding Tax under the National Internal Revenue Code and applicable BIR regulations

The specific tax treatment depends on the nature of the income and the applicable provisions of law.

Why Is It Important?

Form 2306 serves as proof that:

- Final Withholding Tax has already been withheld;

- the tax has been remitted to the BIR; and

- the recipient’s tax obligation on the covered income has generally been satisfied.

It also supports tax compliance during audits and financial reporting.

BIR Form 2316

Certificate of Compensation Payment/Tax Withheld

BIR Form 2316 applies exclusively to employees.

Employers issue this certificate to report:

- total compensation paid;

- taxable compensation;

- taxes withheld from salaries;

- employer information;

- employee information.

It summarizes an employee’s compensation and withholding tax for the taxable year.

Who Receives Form 2316?

Form 2316 is generally issued to:

- Regular employees

- Probationary employees

- Managerial employees

- Rank-and-file employees

- Resigned employees

- Retired employees

- Employees transferred during the year, where applicable

Why Is It Important?

Employees use Form 2316 for:

- substituted filing, where applicable;

- annual income tax compliance;

- visa applications;

- loan applications;

- proof of employment income;

- financial documentation.

Employers are responsible for ensuring that the certificate accurately reflects the employee’s compensation and taxes withheld.

Comparing the Three Forms

Purpose

2307

Supports tax credits.

The tax withheld is creditable against future income tax.

2306

Documents Final Withholding Tax.

The tax obligation on the covered income is generally considered fully satisfied.

2316

Reports compensation income and taxes withheld from employees.

Type of Income

2307

Business income and professional income subject to Expanded Withholding Tax.

2306

Passive income and other income subject to Final Withholding Tax.

2316

Compensation income.

Who Issues the Certificate?

All three certificates are issued by the withholding agent.

Examples include:

- Employers

- Business clients

- Financial institutions

- Corporations

- Government agencies

- Other entities required to withhold taxes

Common Mistakes

Many taxpayers misunderstand these certificates.

Mistake #1: Confusing Form 2307 with Form 2306

Many recipients assume both certificates create tax credits.

They do not.

Form 2307 generally represents creditable withholding tax, while Form 2306 relates to final withholding tax.

Mistake #2: Losing Tax Certificates

Businesses often misplace Forms 2307 or 2306.

Without proper documentation, taxpayers may have difficulty substantiating tax positions during a BIR audit.

Maintain organized records throughout the year.

Mistake #3: Employees Not Reviewing Form 2316

Employees should verify:

- correct TIN;

- correct compensation;

- taxes withheld;

- employer information.

Errors should be corrected before annual filing deadlines.

Mistake #4: Failure to Reconcile Records

Businesses should reconcile:

- tax certificates;

- accounting records;

- income tax returns;

- withholding tax returns.

Inconsistencies frequently lead to audit findings.

Mistake #5: Assuming All Withholding Taxes Are Refundable

Not every withheld tax results in a refundable credit.

Only creditable withholding taxes, supported by the appropriate certificate and applicable legal requirements, may generally be credited against income tax liabilities.

Best Practices

Whether you are an employer, business owner, or individual taxpayer:

Keep Every Certificate

Maintain copies of:

- BIR Form 2307

- BIR Form 2306

- BIR Form 2316

Store both printed and electronic copies whenever possible.

Reconcile Before Filing Tax Returns

Ensure that:

- tax certificates;

- accounting records;

- tax returns;

- financial statements

are consistent.

Verify Taxpayer Information

Check:

- TIN;

- registered name;

- addresses;

- tax amounts.

Small errors may create significant compliance issues.

Work with Your CPA

Tax professionals can help verify that withholding tax certificates are:

- properly issued;

- correctly recorded;

- appropriately reflected in tax returns.

Early review reduces filing errors.

Final Thoughts

Although BIR Forms 2307, 2306, and 2316 all relate to taxes withheld at source, they serve very different purposes. Form 2307 supports claims for creditable withholding taxes on business and professional income, Form 2306 documents taxes that are considered final on specific types of income, and Form 2316 summarizes an employee’s compensation and taxes withheld by the employer.

Understanding these distinctions helps taxpayers file accurate returns, claim legitimate tax benefits, and avoid unnecessary issues during BIR examinations. Businesses should also establish procedures to issue the correct certificates on time and maintain complete records to support future tax compliance.

Proper management of withholding tax certificates is not just good recordkeeping—it is an essential part of responsible tax compliance under Philippine law.

Disclaimer: This article is intended for general informational purposes only and should not be construed as legal or tax advice. The application of BIR Forms 2307, 2306, and 2316 depends on the taxpayer’s specific facts, the nature of the income received, and the applicable provisions of the National Internal Revenue Code, BIR regulations, revenue issuances, and relevant tax treaties. Businesses and individual taxpayers should consult a qualified CPA or tax lawyer to ensure proper compliance with Philippine withholding tax requirements.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply