Many corporations are surprised when they report little or no taxable income but still receive an income tax assessment. The reason is the Minimum Corporate Income Tax (MCIT), a special tax imposed under the National Internal Revenue Code (NIRC) to ensure that corporations with substantial gross income pay at least a minimum level of income tax.

For many business owners, MCIT is often misunderstood as an additional or “penalty” tax. In reality, MCIT is not necessarily a permanent tax cost. When properly monitored and managed, excess MCIT can become a valuable tax asset that may be credited against future income tax liabilities.

Understanding when MCIT applies, how it is computed, and how excess MCIT can be utilized is essential for effective corporate tax planning.

What Is the Minimum Corporate Income Tax (MCIT)?

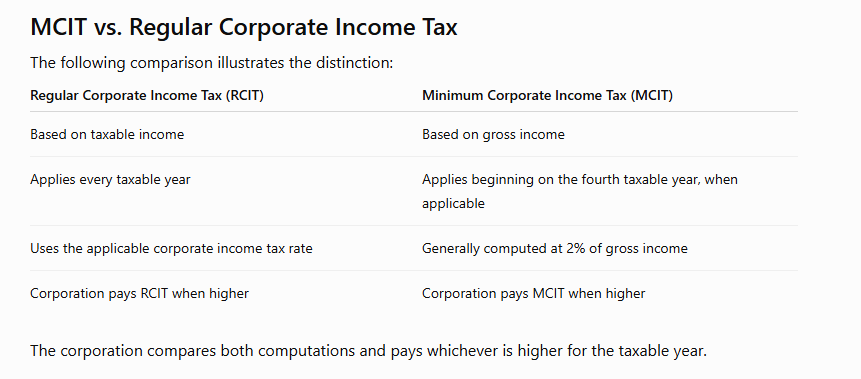

The Minimum Corporate Income Tax (MCIT) is a tax imposed on domestic corporations and certain resident foreign corporations when the MCIT is greater than the regular corporate income tax (RCIT) computed under the Tax Code.

Unlike the regular corporate income tax, which is based on taxable income, MCIT is based on gross income.

Its purpose is to ensure that corporations generating substantial revenues contribute a minimum amount of tax, even if deductions significantly reduce taxable income.

The Tax Code generally imposes MCIT at 2% of gross income, beginning on the fourth taxable year immediately following the year the corporation commenced business operations, whenever the MCIT exceeds the regular corporate income tax. The Maximizing Tax Assets presentation highlights these basic rules.

When Does MCIT Apply?

MCIT does not apply immediately after a corporation is formed.

Instead, it generally becomes applicable:

- beginning on the fourth taxable year following the year business operations commenced; and

- only when the MCIT is higher than the corporation’s regular corporate income tax.

If the regular corporate income tax is greater than the MCIT, the corporation pays the regular income tax instead.

Why Was MCIT Introduced?

The government introduced MCIT to address situations where corporations continuously reported little or no taxable income despite generating significant revenues.

Examples include:

- excessive deductions,

- recurring operating losses,

- aggressive tax planning,

- prolonged reporting of minimal taxable income.

MCIT serves as a safeguard against these situations while still allowing legitimate deductions under the Tax Code.

How Is MCIT Computed?

The basic formula is straightforward:

MCIT = Applicable MCIT Rate × Gross Income

Unlike regular income tax, which focuses on net taxable income after allowable deductions, MCIT is computed using gross income as defined under the Tax Code.

Because of this difference, corporations with low profit margins may still become subject to MCIT even if they earn little taxable income.

When Is MCIT Imposed?

MCIT generally applies when:

- the corporation has zero taxable income;

- the corporation reports a net operating loss; or

- the computed MCIT exceeds the regular corporate income tax.

The Maximizing Tax Assets presentation explains that MCIT may be imposed even where a corporation has zero or negative taxable income if the MCIT exceeds the normal income tax.

Excess MCIT: A Valuable Tax Asset

One of the most misunderstood features of MCIT is that excess MCIT is not automatically lost.

If the corporation pays MCIT because it exceeds the regular corporate income tax, the excess MCIT may generally be carried forward and credited against the regular corporate income tax for the next three (3) taxable years, subject to the requirements of the Tax Code.

This transforms excess MCIT into a tax asset that can reduce future income tax liabilities.

Unfortunately, many corporations fail to monitor these carryovers and lose the benefit once the allowable period expires.

Practical Example

Assume a corporation computes:

- Regular Corporate Income Tax: ₱800,000

- Minimum Corporate Income Tax: ₱1,100,000

Since the MCIT is higher, the corporation pays ₱1,100,000.

The ₱300,000 difference (the excess of MCIT over RCIT) may generally be carried forward and credited against future regular corporate income taxes within the allowable three-year period, provided the statutory requirements are satisfied.

Proper monitoring ensures that this valuable tax asset is not forfeited.

Common Mistakes Businesses Make

Many corporations unknowingly lose MCIT benefits because they:

1. Forget to Track Excess MCIT

Without an annual monitoring schedule, excess MCIT may expire unused.

2. Assume MCIT Is a Permanent Tax

Many business owners mistakenly believe MCIT cannot be recovered.

In reality, properly tracked excess MCIT can reduce future income taxes.

3. Ignore Annual Tax Planning

Corporations often focus solely on the current year’s taxes instead of evaluating future opportunities to utilize excess MCIT.

4. Fail to Reconcile Tax Records

MCIT schedules should always reconcile with:

- Income Tax Returns;

- Financial Statements;

- Deferred tax schedules; and

- Tax working papers.

Poor documentation increases the risk of losing available tax credits during a BIR examination.

Practical Tax Planning Tips

Businesses can maximize the benefits of MCIT by adopting proactive tax management practices.

Maintain an MCIT Monitoring Schedule

Track:

- Year of payment

- Amount of excess MCIT

- Expiration year

- Amount utilized

- Remaining balance

This simple schedule can prevent valuable tax credits from expiring.

Review Corporate Profitability Annually

Forecasting taxable income helps determine whether excess MCIT can likely be utilized before expiration.

Early planning allows management to make informed business and tax decisions.

Coordinate Accounting and Tax Records

Accounting records, tax returns, and supporting schedules should always be consistent.

Proper reconciliation strengthens audit readiness and supports future tax credit claims.

Conduct an Annual Tax Asset Review

MCIT should be reviewed together with other available tax assets, including:

- Creditable Withholding Taxes (CWT)

- Net Operating Loss Carry-Over (NOLCO)

- Excess Input VAT

- Deferred Tax Assets

- Tax Credit Certificates

A comprehensive review helps ensure that no available tax benefit is overlooked.

Final Thoughts

The Minimum Corporate Income Tax is one of the most significant tax provisions affecting Philippine corporations. Although it may initially appear to increase a corporation’s tax burden, excess MCIT can become a valuable tax asset when properly monitored and utilized.

Businesses should not view MCIT merely as an additional tax but as part of a broader tax planning strategy. By understanding when MCIT applies, maintaining accurate records, monitoring excess MCIT carryovers, and integrating MCIT into annual tax planning, corporations can improve cash flow, avoid the expiration of valuable tax credits, and remain fully compliant with Philippine tax laws.

For every corporation, effective tax planning begins not only with minimizing taxes today—but also with preserving tax assets that can reduce taxes tomorrow.

Disclaimer: This article is intended for general informational purposes only and should not be construed as legal or tax advice. The application of the Minimum Corporate Income Tax depends on the taxpayer’s specific facts, applicable provisions of the National Internal Revenue Code, BIR regulations, and prevailing jurisprudence. Consult a qualified CPA and tax lawyer before making tax planning decisions or claiming excess MCIT credits. The discussion is informed in part by the Maximizing Tax Assets presentation.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply