One of the most common mistakes made by taxpayers in the Philippines is filing the wrong Annual Income Tax Return (AITR). Choosing the incorrect BIR form can result in delayed processing, penalties, deficiency tax assessments, and unnecessary compliance issues with the Bureau of Internal Revenue (BIR).

Whether you are an employee, freelancer, sole proprietor, professional, corporation, or partnership, selecting the correct annual income tax return is an essential part of tax compliance.

This guide explains the differences among BIR Forms 1700, 1701, 1701A, and 1702, who should file each form, and how to determine which return applies to your business or profession.

Why Choosing the Correct Tax Return Matters

Every taxpayer has different reporting obligations depending on:

- the nature of income earned;

- taxpayer classification;

- business registration;

- legal structure;

- applicable tax regime.

Using the correct BIR form helps ensure:

- accurate tax reporting;

- proper computation of income tax;

- avoidance of penalties;

- easier processing by the BIR;

- compliance during tax audits.

Filing the wrong return may require amendments and could expose the taxpayer to surcharges and interest if tax liabilities are affected.

Understanding Annual Income Tax Returns

The Annual Income Tax Return (AITR) reports the taxpayer’s total income, allowable deductions, tax credits, and income tax due for the taxable year.

Depending on the taxpayer, the applicable return may be:

- BIR Form 1700

- BIR Form 1701

- BIR Form 1701A

- BIR Form 1702 (including its applicable variants)

Each serves a different category of taxpayer.

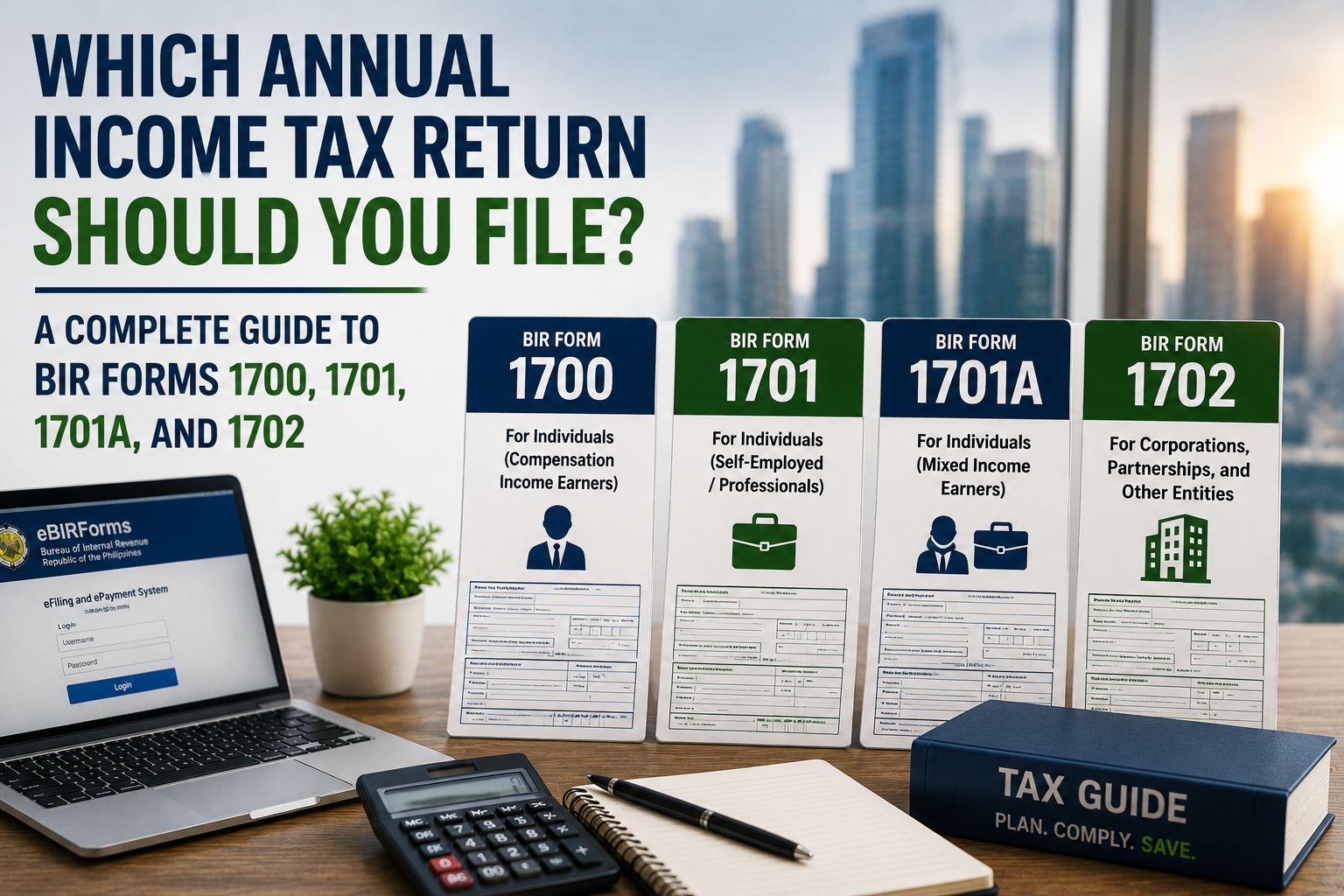

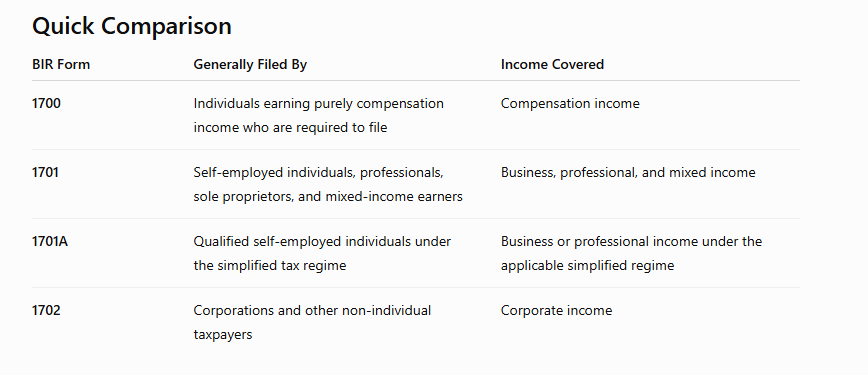

BIR Form 1700

Annual Income Tax Return for Individuals Earning Purely Compensation Income

Who Should File?

BIR Form 1700 is generally filed by individuals earning purely compensation income when they are required to file an annual income tax return.

Examples include employees who:

- have multiple employers during the taxable year;

- are not qualified for substituted filing;

- receive taxable compensation requiring the filing of an annual return.

Who Usually Does NOT File Form 1700?

Many employees do not personally file Form 1700 because they qualify for substituted filing, where the employer files the necessary reports and withholds the correct income tax.

Substituted filing generally applies only if all statutory requirements are met.

Income Covered

Typical income includes:

- salaries;

- wages;

- bonuses;

- commissions;

- taxable allowances;

- other compensation benefits.

BIR Form 1701

Annual Income Tax Return for Self-Employed Individuals, Professionals, and Mixed Income Earners

Who Should File?

BIR Form 1701 is generally used by:

- sole proprietors;

- self-employed individuals;

- licensed professionals;

- freelancers;

- consultants;

- mixed-income earners (those receiving both compensation income and business or professional income), when applicable under current tax rules.

Income Covered

Examples include:

- professional fees;

- consulting income;

- online business income;

- retail business income;

- service income;

- freelance income;

- business profits.

Compensation income, if applicable, is also included for mixed-income earners.

BIR Form 1701A

Annual Income Tax Return for Individuals Under the Simplified Tax Regime

BIR Form 1701A was introduced to simplify annual tax reporting for qualified individual taxpayers.

Who Should File?

Generally, Form 1701A is intended for self-employed individuals and professionals who qualify under the applicable tax regime prescribed by law and BIR regulations.

Examples may include:

- freelancers;

- consultants;

- online sellers;

- sole proprietors;

- professionals who qualify under the simplified income tax options.

Advantages

Compared with Form 1701, Form 1701A generally offers:

- simplified reporting;

- fewer schedules;

- easier preparation;

- streamlined tax computation.

However, not every self-employed taxpayer qualifies.

Eligibility depends on the taxpayer’s chosen tax regime and compliance with applicable laws.

BIR Form 1702

Annual Income Tax Return for Corporations, Partnerships, and Other Non-Individual Taxpayers

Corporations do not use Forms 1700, 1701, or 1701A.

Instead, they file BIR Form 1702, together with the appropriate version applicable to their tax status.

Who Should File?

Generally, Form 1702 applies to:

- domestic corporations;

- resident foreign corporations;

- partnerships taxable as corporations;

- other non-individual taxpayers required to file corporate income tax returns.

Income Covered

Corporate returns include:

- operating revenues;

- investment income;

- capital gains, where applicable;

- deductible expenses;

- tax credits;

- Minimum Corporate Income Tax (MCIT);

- Net Operating Loss Carry-Over (NOLCO), when available.

Corporate taxpayers should ensure that their annual return is consistent with quarterly income tax returns and audited financial statements, where required.

How to Determine Which Form You Should File

Ask yourself these questions:

Are you an employee only?

You will generally use BIR Form 1700 if you are required to file an annual return and do not qualify for substituted filing.

Do you own a business?

You will generally file either:

- BIR Form 1701, or

- BIR Form 1701A, depending on your eligibility and chosen tax regime.

Are you both employed and operating a business?

You will generally file BIR Form 1701, since both compensation income and business income must be reported.

Is your business incorporated?

Corporations generally file BIR Form 1702, not Forms 1700 or 1701.

Common Filing Mistakes

Many taxpayers encounter compliance issues because they:

Filing the Wrong Return

Choosing the incorrect BIR form may delay processing and require amendments.

Assuming Employees Never File

While many employees qualify for substituted filing, some are still required to submit their own annual income tax returns.

Confusing Sole Proprietorships with Corporations

A sole proprietor is taxed as an individual, not as a corporation.

The business owner files an individual income tax return—not Form 1702.

Ignoring Mixed Income Rules

Individuals who both receive salaries and operate businesses often forget that both sources of income may need to be reported in the appropriate return.

Missing Filing Deadlines

Annual income tax returns have statutory filing deadlines.

Late filing may result in:

- surcharge;

- interest;

- compromise penalties;

- possible BIR audit concerns.

Maintaining a tax compliance calendar helps prevent missed deadlines.

Best Practices Before Filing

Before preparing your Annual Income Tax Return:

- Confirm your taxpayer classification.

- Verify your business registration with the BIR.

- Determine your applicable tax regime.

- Reconcile all quarterly tax returns.

- Gather Certificates of Creditable Withholding Tax (BIR Form 2307), if applicable.

- Prepare complete financial records.

- Review available tax credits and deductions.

- Consult a CPA or tax lawyer if your reporting obligations are complex.

Proper preparation minimizes errors and facilitates smoother tax compliance.

Final Thoughts

Selecting the correct Annual Income Tax Return is one of the first and most important steps toward tax compliance in the Philippines. Whether you are an employee, freelancer, sole proprietor, professional, or corporation, understanding the purpose of BIR Forms 1700, 1701, 1701A, and 1702 helps ensure accurate reporting and reduces the risk of costly mistakes.

Because tax obligations vary depending on the taxpayer’s legal structure, income sources, and chosen tax regime, there is no one-size-fits-all approach. Filing the correct return, maintaining complete records, and reconciling income and tax credits throughout the year can help businesses and individuals remain compliant while maximizing legitimate tax benefits.

When in doubt, seek professional advice before filing. Choosing the correct form today can save you significant time, money, and compliance issues in the future.

Disclaimer: This article is intended for general informational purposes only and should not be construed as legal or tax advice. The appropriate Annual Income Tax Return depends on the taxpayer’s specific facts, registration status, income sources, applicable tax regime, and prevailing BIR regulations. Tax laws and BIR forms may be amended from time to time. Consult a qualified CPA or tax lawyer to determine the correct return to file and to ensure full compliance with Philippine tax laws.

Navigating the business landscape in the Philippines can be both rewarding and intricate. Whether you’re embarking on a new venture or scaling up, ensuring that your corporate endeavors are in line with local regulations is paramount.

At CBOS Business Solutions Inc., we pride ourselves on simplifying these processes for our clients. As a seasoned professional services company, we offer comprehensive assistance with SEC Registration, Visa processing, and a myriad of other essential business requirements. Our team of experts is dedicated to ensuring that your business is compliant, well-established, and ready to thrive in the Philippine market.

Why venture into the complexities of business registration and compliance alone? Allow our team to guide you every step of the way. After all, your success is our commitment.

Get in touch today and let us be your partner in achieving your business goals in the Philippines.

Email Address: gerald.bernardo@cbos.com.ph

Mobile No.: +639270032851

You can also click this link to schedule a meeting.

Leave a Reply